ICONIQ.

in 1984, two talents were born.

In January 2011, Goldman Sachs invested $1.5 billion into Facebook, roughly a year before the social media giant’s IPO, at a $50 billion valuation.

In addition to a $450 million principal investment, Goldman Sachs also created a special purpose vehicle (SPV) with the intent of giving their private wealth clients access to the hottest company in the world. Goldman looked to fill the SPV with the outstanding $1 billion.

For some reason, Goldman’s email to their clients did not mention the company (Facebook) by name, and when the suspicious client email got leaked to the media, the SEC started digging around. Goldman folded. Under SEC rules at the time, private placements came with a strict prohibition on mass solicitation, and not mentioning the company by name, as well as using language like the “opportunity of a lifetime”, gave regulators the impression that Goldman was trying to pull a fast one. Goldman ended up filling the SPV with foreign dollars to avoid further scrutiny, but the damage was done - Facebook was embarrassed. The most prestigious investment bank in the world would no longer be the lead bookrunner for Facebook’s IPO.

One of the most notable fumbles in modern investment banking.

Morgan Stanley went on to be the lead-left bank, JP Morgan was second, and Goldman Sachs fell to third.

Divesh Makan was technically working at Morgan Stanley at the time. Well, he actually had a history working for Goldman Sachs as a wealth advisor in San Francisco, a job he took after a Wharton MBA in 2001. Makan wanted to do investment banking or private equity, but the job market was tough post-dot-com bubble. He made the most of his Goldman gig, hustling to meet the next big tech entrepreneurs in the Bay Area before they became big fish. He met Mark Zuckerberg around 2004, when Facebook first landed in Palo Alto. While at Goldman, Makan was known for going above and beyond the typical wealth advisor duties, often helping clients with the extracurriculars such as doing business school applications for clients’ kids and planning bachelor parties. This full-service style approach is considered acceptable at private family offices, but Goldman’s stiff structure meant Makan butted heads with the compliance team and colleagues at several points during his tenure. In 2008, he was fired for a “loss of trust”, according to representatives at Goldman Sachs. Makan has publicly stated that he left over a “workplace disagreement.”

Morgan Stanley picked him up quickly, paying a reported $20 million signing bonus to get the deal done. Chad Boeding and Michael Anders, two of his trusted colleagues at Goldman, followed him to the new platform. As Zuckerberg and other high-profile tech execs began to grow in stature, Makan’s network became a highly legible asset to the Morgan Stanley wealth business. Zuck was getting wealthier each year, and Makan was his primary advisor. The trio had more autonomy at Morgan Stanley, but there was still friction. In 2011, when it became crystal clear that Facebook was going to be one of the most valuable IPOs of all time, higher-ups at Morgan Stanley made plans to give Makan the wealth management equivalent of Frank Quattrone’s deal at CSFB, with the aim of retaining Zuckerberg and other Facebook executives in as wealth management clients. But Makan, obviously a student of the game, decided to walk away from Morgan Stanley in his prime and build a family office platform around Mark Zuckerberg. Anders and Boeding joined, and they launched Iconiq at the same time as the Facebook IPO, which Morgan Stanley led.

This is a story about how Makan’s decision to leave Morgan Stanley spiraled into a $100 billion platform.

The United States is expected to experience a financial advisor shortage in the next ten years.

A report from McKinsey estimates that by 2034, the advisor workforce will decline to the point where the industry faces a shortage of roughly 100,000 advisors. For context, there are roughly 300,000+ active advisors in the U.S. right now. The industry is heavy with older professionals, and retirement is outpacing recruitment, as graduates are steering away from the field.

On a firm level basis, there are 15,000+ SEC registered investment advisor (RIA) firms in the U.S.

The most common business model for an RIA is to charge ~1% of assets under management (AUM), and the percentage typically decreases as the amount of assets go up, to incentivize larger accounts. The median RIA manages ~$393 million and has 8 employees. To break into the top 5% of RIAs, a U.S. based firm must crack the $1 billion assets under management mark. At $10 billion assets under management, a U.S. based firm is now flirting with top <0.2% status, safely within the top 50 largest RIAs in America.

Within the upper stratosphere of wealth managers, there are two dominant strategies.

The “mass-affluent” model focuses on relationship quantity, drawing in tens of thousands of clients who have, from a wealth management perspective, smaller accounts and thus lower margins for the platforms that manage them. Some examples of firms in the mass-affluent space include Moneta ($37 billion AUM, ~$900,000 average account size, ~41,000 clients) and Savant ($26 billion AUM, ~$1.7 million average account size, ~15,000 clients).

The “UHNW” model focuses on relationship depth, usually measured by lofty average account sizes and breadth of services. This model prioritizes selectivity and going above and beyond for the select clients they work with. Circle Wealth ($10 billion AUM, ~$11 million average account size, <1,000 clients) is a good example.

Iconiq is the most extreme version of the UHNW model, with somewhere around $70 billion AUM across less than 300 families, implying an average account of more than $230 million. It is, perhaps, the most capital efficient RIA in modern history, the most concentrated formal network of wealth in America, and the most valuable brand in the industry.

Although $70 billion is a reasonable estimate of RIA AUM, this number is tricky to pinpoint given Iconiq’s opaque nature. On public materials, the firm lists $100 billion AUM, but this number includes both the wealth management and investment arm. In 2024, a Fortune article reported that Iconiq had $60 billion AUM on the wealth side and $20+ billion AUM on the investment side, for a total of $80+ billion total assets under management. No matter how you slice it, Iconiq is a case study worth examining closer.

When Makan, Boeding, and Anders split from Morgan Stanley, they did so on good terms with their former employer. On day one, Iconiq actually struck a deal with Morgan Stanley Wealth Management for back office support and proprietary deals. The launch came with approximately $1 billion across roughly a dozen clients, and within two years of launch, scaled to $7 billion across roughly two dozen clients. The foundation to their growth was, at first, Mark Zuckerberg, and then, the Iconiq network. Mark Zuckerberg as a founding client opened every door they wanted. The easy thing to do after bringing Zuck on would have been to optimize for the quantity of accounts above a set threshold, for example, a $15 million account minimum. But the doors to Iconiq remained closed, open only to the top dogs in technology, finance, and entertainment. Over time, guys like David Bonderman (TPG founder), Jack Dorsey (Twitter, Block founder), Henry Kravis (KKR founder), Satya Nadella (Microsoft CEO), Will Smith, Ashton Kutcher, and Justin Timberlake signed up as Iconiq clientele. And to provide palatable contrast to their high profile accounts, the firm remained as lowkey as possible.

The question is, why is there only one Iconiq? Surely, a number of extraordinary entrepreneurs exist outside of Mark Zuckerberg… Where are the other Divesh Makans at GS/MS/JPM that have a single highly valuable relationship and can spin out into their own shop? By the end of this piece, the answer will be clear. But first, the most notable basketball executive you’ve never heard of…

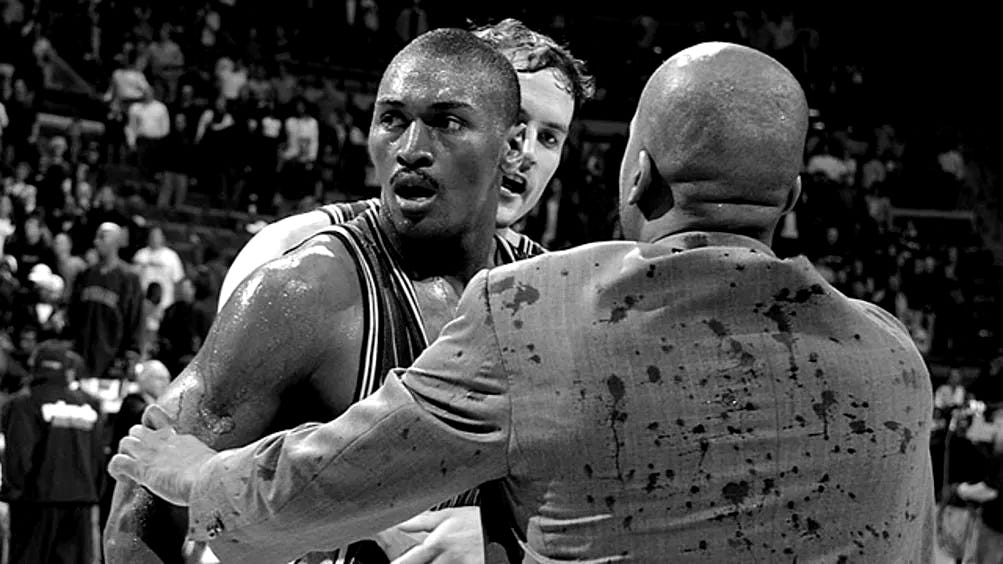

Malice in the Palace will forever be remembered as the modern NBA’s most violent night. A hard foul by the Pacers’ Ron Artest on the Pistons’ Ben Wallace escalated into a brawl, then fans got involved, and Ron Artest rushed the stands in an attack on a fan that threw a drink at him. Stephen Jackson followed, punches were thrown, and utter chaos ensued.

Ron Artest was suspended for 86 games afterwards and lost $5 million in salary.

In the midst of this black swan event was a man with no formal affiliation to the Pacers, the Pistons, or Ron Artest. The man in the gray suit pictured below is William Wesley, one of the most powerful men in basketball, popping up out of nowhere to try and restrain Artest.

Wesley grew up in Cherry Hill, New Jersey, and as a teenager, worked at Pro Shoes, a high-end sneaker shop. He would use the gig to build a network of basketball royalty, from up and coming high school stars like Milt Wagner to current NBA players on the Nets and 76ers. In the early 1990s, Milt Wagner, now an NBA player, introduced Wesley to Michael Jordan. Jordan gave Wesley a job at his basketball camp, and by 1993, he moved out to Chicago full time. In Chicago, Wesley became friends with the Clintons, Phil Knight, basketball executives, and anyone in between. William Wesley has been credited for brokering peace between 76ers coach Larry Brown and star player Allen Iverson, helping John Calipari land high school phenom Dajuan Wagner, and building Creative Artists Agency into a basketball powerhouse.

His most notable feat is as follows. Aaron Goodwin is from Oakland, California. Which means he had a front seat to watching Lebron James dominate the AAU circuit as a member of the Oakland Soldiers. Goodwin built a relationship with Lebron’s family in high school and ultimately won the right to represent him in May 2003, right before the NBA draft. From a distance, Wes watched and observed. Well, actually, Wes was pretty close to the action. Wes became friends with Lebron’s surrogate father, Eddie Jackson, built a friendship with Lebron himself, and eventually introduced Lebron to Jay-Z, a dream come true for the young hooper. In 2003 Wes moved to Cleveland for proximity. In 2005, Lebron cut ties with Goodwin and signed with Leon Rose, who, less than two years after, moved his business to CAA. Rose almost exclusively represented players that had ties to Wesley. And, important to note, Leon Rose was William Wesley’s lawyer; the two grew up in New Jersey together. CAA signed Wes as a “consultant” and became the default agency for basketball superstars. This is the story of how “Worldwide Wes” put CAA on the basketball map for good.

The relevant part of this story, however, as it pertains to Iconiq, takes place in 2012, around the same time that Facebook went public. On September 13, 2012, Lebron left CAA, and Leon Rose, to be managed by his longtime friend, Rich Paul, who, without coincidence, was a former CAA employee under Leon Rose. The timing was critical, Lebron just won his first championship, was coming off an MVP season, and was, without reasonable doubt, the best player in the world. Paul was a childhood friend of Lebron’s and learned the game from William Wesley. At the peak of Lebron’s power, the two decided to start a platform of their own, in the same year that Facebook went public and Makan-Zuckerberg made an analogous move.

Klutch Sports, Rich Paul’s agency, now manages $7 billion in athlete contracts, and has expanded past basketball. Clients include Lebron James, Jalen Hurts, Tyrese Maxey, Anthony Davis, Draymond Green, Odell Beckham Jr., Myles Garrett, and more. Klutch is a top five agency in North America by contract value and commissions.

The key reason why Klutch worked so well is because there is only one Lebron James, and the move was made in his prime. Outside of Michael Jordan and perhaps Kobe Bryant, James is the most high profile NBA player of all time, and Rich Paul was able to capitalize on this right after he won his first championship. Klutch probably wouldn’t work as well if it were founded today. Timing was of the essence. This was Lebron’s IPO equivalent.

With that in mind, it’s important to understand just how dominant Zuckerberg’s run was in the early 2000s.

Facebook was the most highly valued tech startup in history leading up to its IPO.

And it was being run by a 28 year old Zuckerberg the year of its IPO, the same year that Lebron won his first championship.

Prior, Zuckerberg became the world’s youngest self-made billionaire at age 23, the same age that Lebron won his first scoring title.

From 2005 to 2012, Zuck set the precedent for founder control:

2005: Series A by Accel, $13 million at ~$100 million valuation

2006: Series B by Greylock, $27 million at ~$527 million valuation

2007: Microsoft Strategic Investment, $240 million at $15 billion valuation

2009/2010: DST Growth, $200 million at $10 billion, $500 million at $15 billion

2011: Goldman Sachs, $1.5 billion at $50 billion valuation

Raising $2.5B before an IPO was unheard of before Facebook, but the most ludicrous part was Zuckerberg’s infamous ownership structure. Before the IPO, he owned 28.4% of the company yet controlled 56.9% of voting power through the dual-class share structure he instituted in 2009, designed to prevent investors from ever ousting him.

Zuckerberg walked so Kalanick, Neumann, Chesky, and Altman could all fly private.

And to cap it all off, this was Zuckerberg’s first company. He had no experience prior to founding Facebook, he is the startup equivalent of going straight from high school to the league. This is a significant part of the reason why Iconiq worked; there were no enduring business relationships Zuck had built from selling past companies or working under others, Makan was the only advisor that was there to take a chance on him early, and when Makan decided it was time to leave Morgan Stanley, Zuck followed suit.

In 2013, roughly a year after Iconiq launched, Dave Goldberg encouraged Divesh Makan to launch an investment arm alongside the wealth advisory brand. Dave was a technology executive and husband to Iconiq client and Facebook COO, Sheryl Sandberg. Goldberg went on to recruit Will Griffith, a longtime venture investor at TCV, to join Iconiq and lead the venture efforts. Iconiq launched its first growth fund that year, a $509 million vehicle, with 67% of investors coming from the wealth management side.

The strategic thinking was pretty sharp. Many of our clients are the biggest names in technology and top founders already want them on cap tables. Our clients also dabble in venture investing and come to us for deal introductions, so why not launch a fund to make things more straightforward? We’d win any deal we want, because who’s going to say no to Mark Zuckerberg and Jack Dorsey? Growth stage also reduces risk and allows for larger check sizes. The fee structure is more favorable, an additional 20% through carried interest, as opposed to just the 1.5% fee that Iconiq charges clients for public markets action.

With every advantage comes disadvantage, and from the perspective of other wealth managers, the disadvantage was too obvious to ignore. Iconiq operating a private investment fund that they shop to their wealth clients is a blatant conflict of interest. A wealth manager is, by SEC’s RIA rules, required to adhere to the fiduciary standard, which necessitates a manager acting in his client’s best interest. Other wealth managers offer a few select funds and allow clients to choose. While Iconiq theoretically does something similar, they are conflicted and incentivized to push forward their own products, and this has only gotten more pronounced as the firm added other asset classes in addition to venture/growth, such as real estate. The reason Iconiq is legally allowed to operate in this gray area is because of their full disclosure to clients that they are indeed “conflicted.” Makan, obviously a student of the game, graduated with honors from Goldman Sachs and Morgan Stanley. Chad Boeding, however, one of Iconiq’s founders alongside Divesh Makan and Michael Anders, actually decided enough was enough. In 2018, Boeding left Iconiq to found Epiq Capital - he couldn’t resist the -iq ending - and cited his reason for leaving Iconiq as “an intense commitment to avoiding conflicts of interest commonly found at major banks and large advisory firms.” Boeding scaled Epiq to $5.9 billion in assets and then sold the firm to IEQ Capital in 2024.

In 2013, Iconiq did a limited number of deals: SurveyMonkey’s $800 million growth round, Flipkart’s Series E, The Honest Company’s $25 million Series B, and Modern Meadow’s $2.5 million seed round. In 2014, the firm tripled the amount of investments made, deploying capital into twelve deals and ten unique companies. 2015 saw a similar amount of deals, 13, with a critical Series A investment in Figma, done at a $77 million valuation.

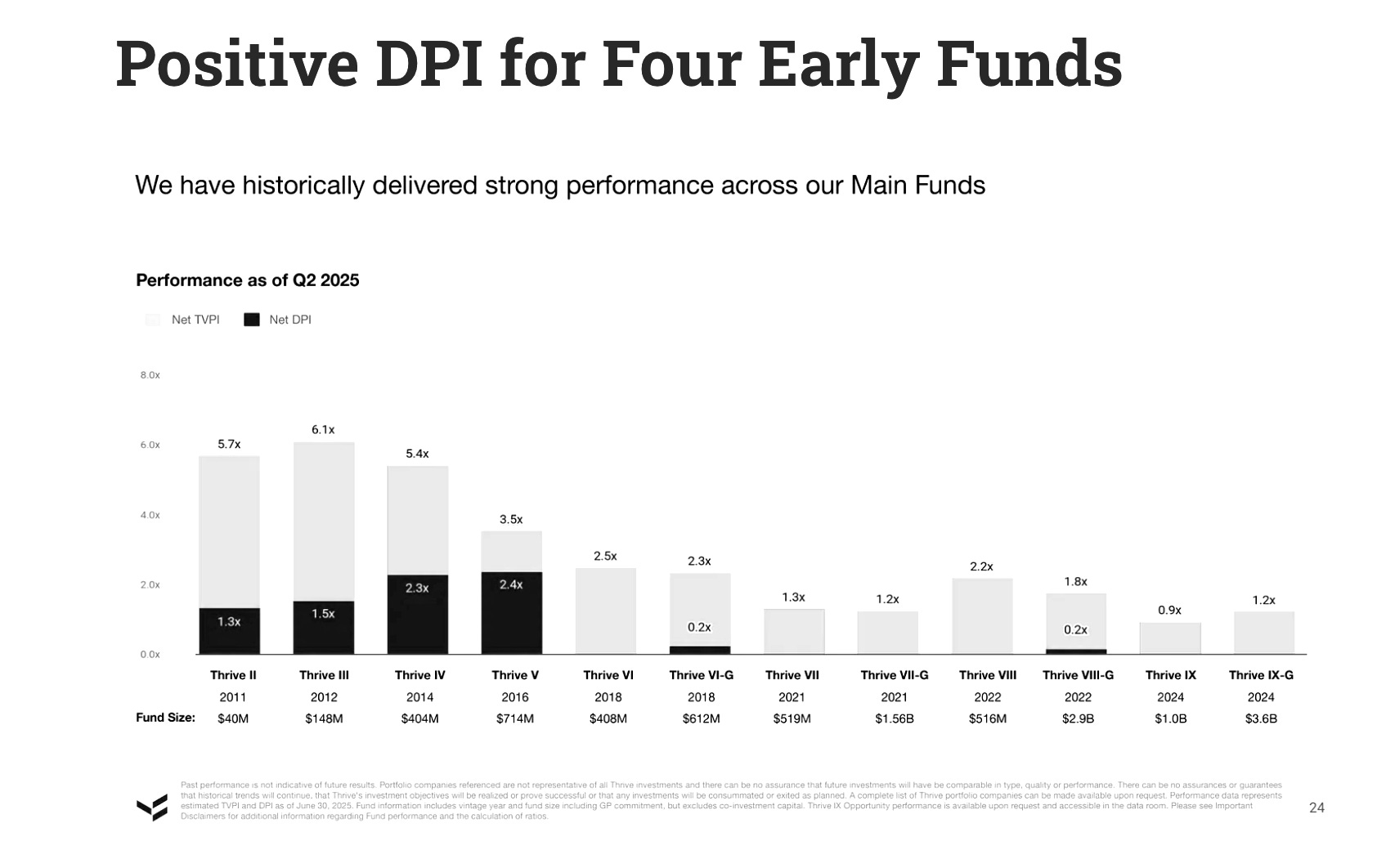

The funds have overperformed, especially considering the focus on growth, which typically warrants a lower return profile:

2013: 2.7x MOIC

2014: 5.5x MOIC (top-decile)

2017: 5.4x MOIC (top-decile)

2019: 1.9x MOIC

Consider top-tier fund Thrive Capital and their early returns, albeit TVPI, not MOIC:

For the early funds, 2013, 2014, and maybe even 2017, MOIC and TVPI should be relatively comparable, as these funds should be mostly or completely realized. TVPI for a given fund is lower than MOIC until full realization, so Thrive is ever so slightly disadvantaged in this comparison. But all of that to say, Iconiq is not simply “Zuck’s family office” anymore. The numbers tell a clear story: Iconiq took their advantage and turned it into a top growth equity platform. Back-to-back 5x funds on $500+ million pools, closed on a $6 billion fund in 2024, and attracted so much demand for their last fund that the proportion of LPs from the wealth arm withered to 20%.

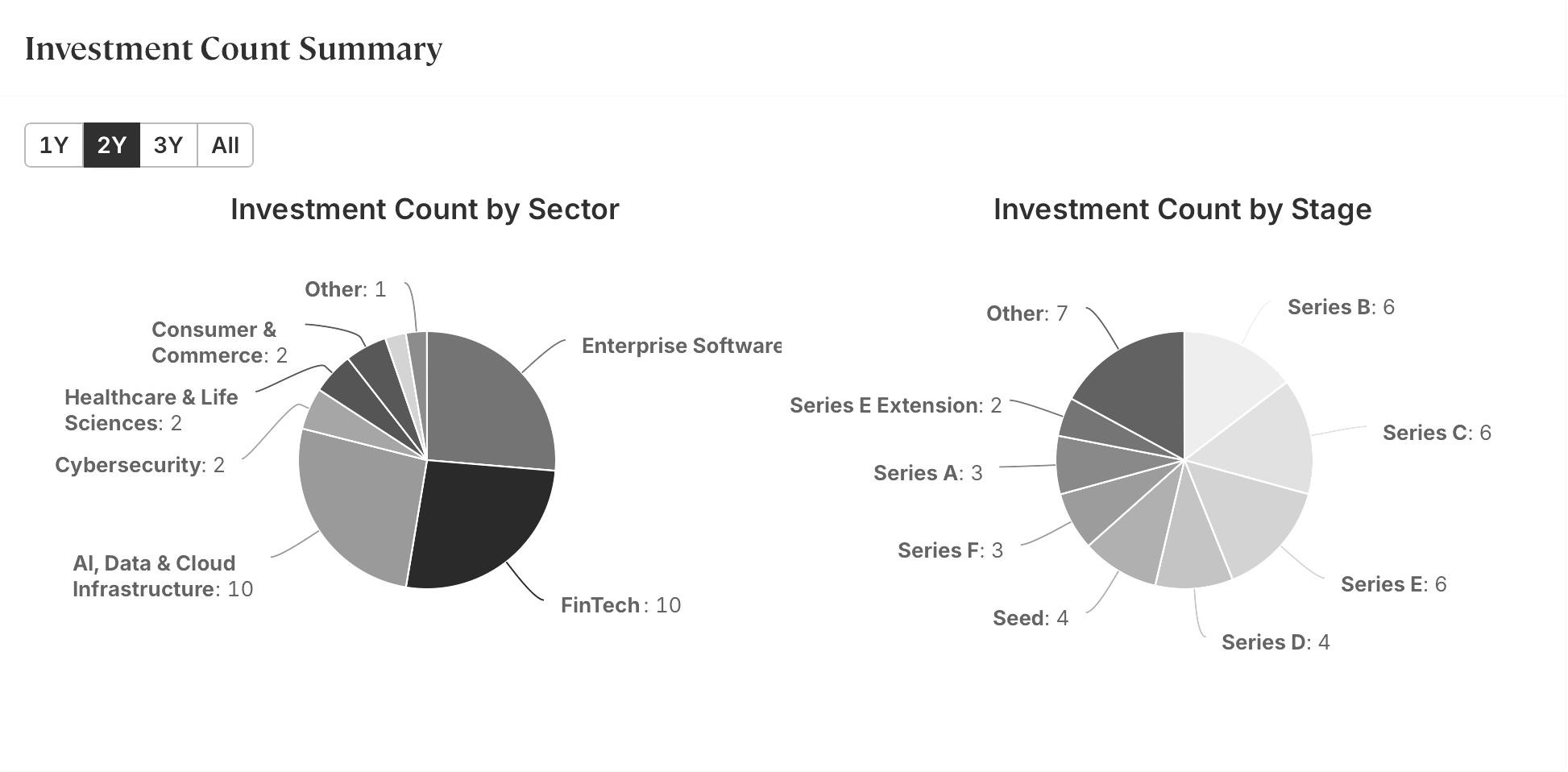

Nowadays, Iconiq has been focusing heavily on both artificial intelligence and financial technology.

Stage-wise, they are flexible as ever, investing from seed to Series F and beyond. Most of their activity is clustered in the B, C, and D rounds.

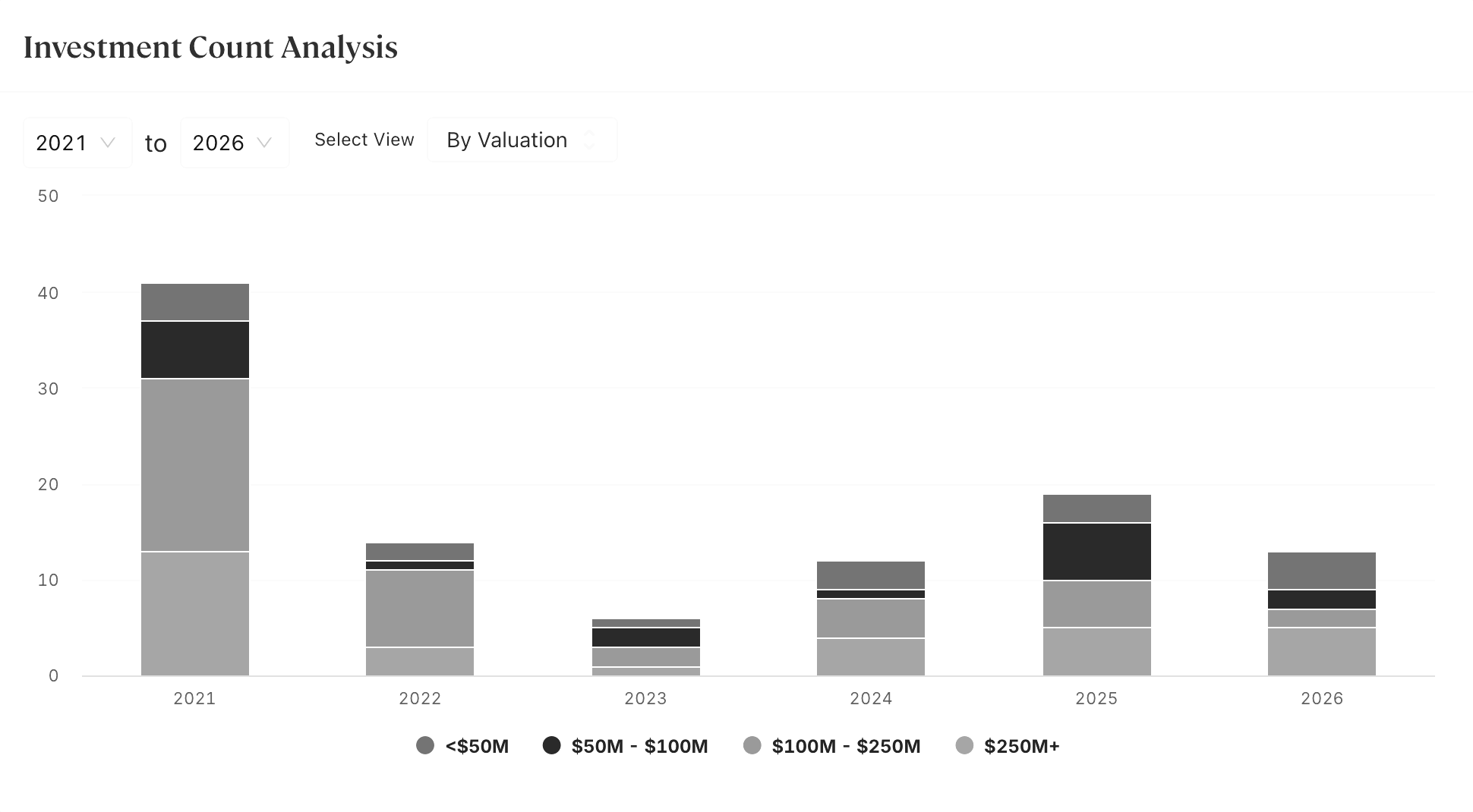

Something interesting to watch is how active Iconiq has been in the first few months of 2026. So far, they’ve already done more volume wise than entire previous years - 2023 and 2024.

This year they’ve led 8 rounds:

Whirl AI | $9 million seed round

Standard Template Labs | $49 million seed round

Quince | $500 million Series E round

Grotto AI | $10 million seed round

Braintrust | $80 million Series B round

Outtake | $40 million Series B round

Rain | $250 million Series C round

Swap | $100 million Series C round

Time flies. Over the course of fourteen years, Iconiq evolved from a boutique RIA with a growth equity arm to a multi-faceted investment firm managing more than $100 billion. No thesis, no stage focus, no financial engineering, just a network that had Zuckerberg as the central node, quite literally the Klutch Sports of technology investing. From that initial network foundation, Makan built various structures to capture value, embraced conflicts of interest without any remorse, and delivered highly respectable returns to his clients, white glove style. Klutch is now built to outlast Lebron, and perhaps even Rich. Only time will tell what Iconiq’s next chapter holds. Now onto a more explosive subject

🏅💡