Under the Bridge II: Name Game

A colorful journey inside the world's largest hedge fund.

Harry Payne Whitney was the grandson of William C. Whitney (former U.S. Secretary of the Navy) and married into the Vanderbilt family through Gertrude. He built a $24M fortune during his life (~$400M+ today). Fun fact, Harry was a thoroughbred horse breeder and dominated the circuit for years on end, winning all three Triple Crown races at various points. Whitney was a Yale alum and spent a lot of time influencing decision making at his alma mater.

Gertrude Vanderbilt Whitney was the daughter of Cornelius Vanderbilt II’s son, and a member of the ultra wealthy Vanderbilt dynasty. She inherited $15M+ in the early 1900’s (~$500M today) from her father and other family estates. She also founded the Whitney Museum of American Art when the Metropolitan Museum rejected her collection of 500 modern works.

Barbara Whitney, Ray Dalio’s girlfriend, was working at the Whitney Museum when he met her.

Two years after they met, they married.

At the time, the Vanderbilt fortune was falling apart.

Barbara let Ray manage what was left of her share.

Dalio’s proximity to generational wealth allowed him to start thinking about investing differently. He realized that extremely wealthy families were much more worried about losing money than making it. Preservation took precedence over rapid gains. The same principles guided stewards of capital at the largest institutions: endowments, pension funds, and the like.

Conservatism was the name of the game. Steady long-term growth was their flex.

It had been almost three years since Dalio first went to Leib for money to seed his import-export business. The business was called Bridgewater, a name that embodied the physical movement of commodities across oceans. Bridgewater was almost three years old without anything to boast of. Ray had lost money for Leib’s connections and went on to manage a modest amount of capital for Barbara.

Bridgewater’s first big break was advising large conglomerates - namely McDonald’s and Nabisco - on commodity futures. Without laboring too heavily over details, Ray told companies who were sensitive to price fluctuations in food inputs (corn, soybeans, etc) to buy financial instruments that would protect them from price increases. At the time, McDonald’s was getting ready to launch chicken nuggets but couldn’t stomach the volatility of chicken prices. Ray explained that the primary driver for chicken price volatility is the price of chicken feed, which consists of soybeans and corn. When farmers pay more for chicken feed, they will naturally increase the price of chickens. Ray’s solution = buy commodity futures to hedge risk.

McDonald’s introduced McNuggets to the world as a result.

Dalio’s work with blue chip corporates opened the door for various roles advising ultra-wealthy individuals. He began to write a newsletter along with other research deliverables that he sold to clients for $3,000 a month. By 1982, he was starting to get the exposure he believed he was owed.

He saw opportunity coming around the corner that year.

The economic climate was dreary. Gold was spiking. Unemployment trending upwards. Interest rates were hiked up to 20%. A recession was taking place. In an effort to garner more publicity, Dalio decided to become the face of doomsday.

He predicted an economic collapse that would make the Great Depression look joyful in comparison. First stop, an interview with The New York Times, then a joint committee at Congress, followed by a TV segment on Wall Street Week.

For his final tour date, Dalio was scheduled to give a speech to the Contrary Opinion Forum.

The market hit bottom three weeks before his speech, and the recession ended.

He lost his clients and cut all of his staff.

He was thirty three at the time.

Reinvention was not a new concept for Ray. He’d done it time and time again, going so far as to change his last name in order to engineer a desired reaction from others.

Now he just needed to find a new lane to channel his drive.

The newsletter ended up bringing more business through the door, and after a dry spell, Dalio got connected with Hilda Ochoa-Brillembourg, Chief Investment Officer for the World Bank pension fund. The two bonded over their shared alma mater. After getting comfortable with her discomfort about Ray’s track record, Hilda agreed to invest $5M into a fixed income portfolio managed by Bridgewater. For a 0.2% annual fee, or 10x lower than the market rate.

Fast forward a few years.

World Bank’s $5M commitment opened the door for new clients, and Bridgewater Associates had $20M AUM.

Ray went back on road to try the depression tour thing one more time.

In February 1987, Ray told Forbes that America only had another year until the crash.

In October 1987, Black Monday took place, and stocks dropped 23% in a single day.

Black Monday was the biggest one-day drop in the U.S. stock market.

Bridgewater ended the year up 27% after going short on equities and long on Treasuries.

The start of a new decade would bring a new dimension to Bridgewater’s growth. It had been more than fourteen years since Ray first started Bridgewater. Construction was coming to a close and it was now time to unveil the architectural masterpiece that was once a figment of his mind.

Hedge funds were all the rage in high finance.

After the crash of 1987, institutional investors were in search of absolute returns that were market neutral.

Pension funds, family offices, and endowments began allocating to hedge funds in the 90’s.

Swensen, Yale’s endowment head, led the wave of elite endowments writing checks to hedge funds, and by the end of the decade, ~15% of Yale’s portfolio was invested in hedge funds.

Between 1985 to 1995, U.S. hedge fund AUM went up nearly 6x

Bullet points don’t do it justice, fund managers were making a killing.

George Soros was the face of hedge fund glory. He founded the Quantum Fund in 1979 and it had ballooned to ~$10B AUM by 1992. Soros and his chief strategist, Stanley Druckenmiller, were paying close attention to European monetary tension. The U.K.’s participation in the European Exchange Rate Mechanism seemed to be a point of weakness considering the rising unemployment, stagnant growth, and broadly weak macroeconomic conditions. The team at Quantum began to short the British pound aggressively, using forward contracts, currency options, swaps, and other financial instruments. Most of the instruments were shorting the British pound against the Deustche mark, which Soros saw as the stronger currency. Quantum gradually built up a deep position using leverage to enhance their bet.

On September 16, 1992, the Bank of England raised interest rates and spent billions trying to defend its currency from Soros and other hedge funds at the door. Too late

Soros had a $10B position by then. He made $1B in profit, secured a spot in finance history and broke the Bank of England in the process.

It took Dalio some time to truly conceptualize a product that would allow him to play with the big boys.

After some thought, he decided to position the fund as a safer investment than, say, Soros’ Quantum Fund. The fund would be based on an investment system that limits downside and provides strong risk-adjusted returns rather than hitting home runs. His intuition came from a decade of experience as well as the initial insight from when he first started working with institutional investors: preservation outweighs growth.

Soros could be Michael Jordan and Larry Bird combined for all he cared. He would be Kareem, a testament to longevity and the fundamentals. Dalio would call it Pure Alpha.

World Bank said no.

Kodak said yes. The photography giant’s pension fund threw in $11M and Pure Alpha was in business.

The first few years showed signs of elite performance:

1993: Pure Alpha = 32%, market = 7%

1996: Pure Alpha = 34%, market = 20%

The equally impressive feat was its risk-adjusted return; you see, Pure Alpha almost never lost money, even when the market took a tumble, because of its institutional grade diversification. Sometimes the markets outperformed Pure Alpha, but investors were willing to stomach that because of the flagship’s ability to limit downside.

Pure Alpha doubled in size almost every year, eventually reaching $3B AUM by 1999.

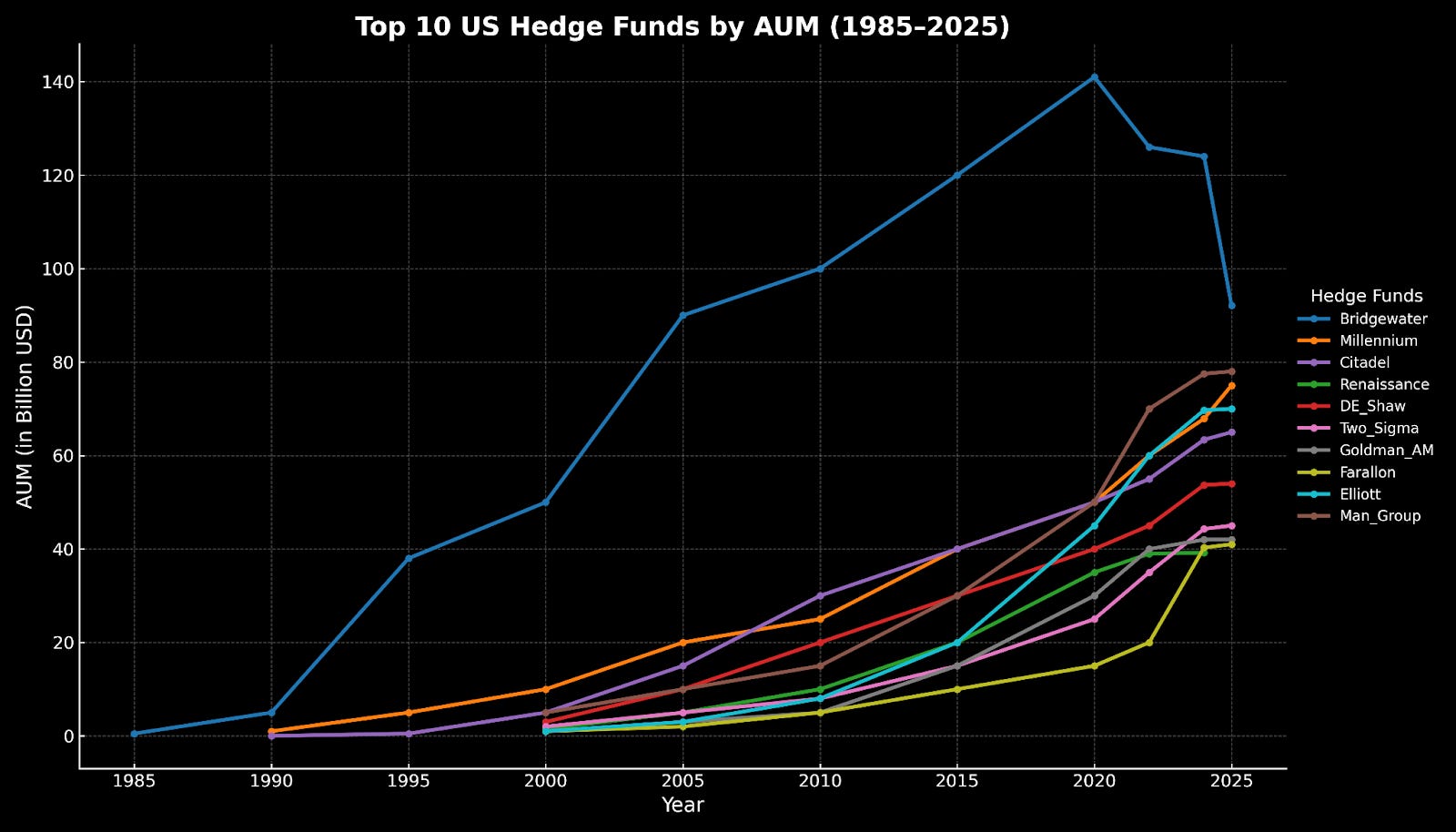

The early 2000’s gave way to evergreen growth, and by 2005, the fund’s assets eclipsed $100B, making Bridgewater the largest hedge fund in the world.

Dalio began to shift his focus to creating a set of rules for management.

He would call it: Principles.

In Season 3, Episode 1 of Black Mirror - “Nosedive” - Lacie is a young woman living in a dystopian world where people can rate each other on a scale from one to five stars, using their smartphones. The ratings are based on each interaction they have - essentially, a decentralized social credit system that impacts their economic well-being. Lacie wants to get her rating up from a 4.2 to a 4.5 so that she can get a discount on a high rise apartment.

The episode ends exactly how you think it will - chaos.

Dalio implemented a similar scheme; the Bridgewater employee-to-employee rating system revolved around virtual “baseball cards”. Employees would rate each other in real time, in a process called dotting, on a 1 to 10 scale. A rating from a highly ranked employee carried more weight. No one was rated as high as Dalio, whose rating was perfect.

Low rated employees were constantly on edge, liable to be let go by management at a moment’s notice.

A social credit system wasn’t enough.

Dalio and his team of ex-military intelligence hires planted hidden cameras and microphones throughout the entire Bridgewater campus.

He had an entire team scraping through surveillance footage 24/7, flagging everything from analysts leaving early to gossip about executives.

When Dalio found something unsatisfactory with an employee, he’d call for an all-hands meeting and have the employee sit at one side of a conference table, with him at the other. He’d rattle off a list of failures, then ask the other attendants whether or not the employee was guilty. It was almost always unanimous agreement with their boss, and it almost always ended in tears from the defendant.

At one point, Greg Jensen was in position for a promotion to the CEO spot. Dalio had been considering stepping down for years, but kept pump faking. After years of pent up frustration, Jensen let his guard down and told another executive - Eileen Murray - that Dalio was a nutcase.

Ray is crazy.

Greg Jensen, Bridgewater CIO, to Eileen Murray

It took just a few days for the Bridgewater militia to report the incident - backed up with video evidence - of the attempted coup.

Dalio quickly called for an all-hands meeting, filling the room with his loyalists and all the evidence necessary to justify the violence that would transpire.

The team went into the “Transparency Library" to find additional recordings of Jensen speaking about Dalio behind his back, then sent firm-wide emails with the findings. Dalio read Jensen a list of all of his wrongdoings since the firm’s inception.

After enough time in the torture rack, Jensen broke. He wept and asked for forgiveness.

The one thing Bridgewater employees didn’t have to worry about was getting interrogated for weak investment performance… Because no one outside of Dalio’s inner circle had any investment responsibilities.

Listen, I know what you’re thinking. There’s no way the world’s largest hedge fund hired 900+ employees (now ~1,300) and none of them were investors.

Around 20% of employees were assigned to either investment research or investment engineering, which helped build the data driven allocation engine. But the investment analysts doing research were no more than paid actors, a placebo group in the mad scientist’s lab. Most of the researchers did work that resembled an undergraduate level economics research class. They studied economic history and wrote papers for Dalio to review, and occasionally, their work would be highlighted in a Bridgewater memo. But none of this impacted Bridgewater’s investing in the slightest bit.

Less than ten people had any say at all on investing decisions, which took place behind a series of closed doors that normal employees barely knew about. These individuals were quietly chosen from loyalists who had started as investment associates and spent years at the firm, enduring the toil and never speaking badly about the Bridge. Every one of these people had only ever worked at Bridgewater.

Dalio and Jensen would bring potential members into their office and give them a choice. You can enter into the inner machine of the matrix, but you have to sign a lifetime contract and swear to never work at another trading firm. The handful of invitees gave their lives to the bridge.

Their secret group of investors became known as the “Circle of Trust”.

The few good men who got inside of the machine quickly realized how simple the investing engine was.

Pure Alpha invested using a set of if-then statements that could be run in an Excel sheet

ex.1: if interest rates decline in a country, then Pure Alpha bets against the currencies of the country with falling interest rates

ex.2: if money in circulation shrank, then Pure Alpha sells gold

A lot of the rules for investing implied short term movement was indicative of long term movement

The fundamental money maker for Bridgewater was economic collapse: the worst recessions often led to the firm’s best years. Pure Alpha gained 9% in 2008 while the S&P 500 lost 37%.

Dalio’s Circle of Trust confidantes tried their best to convince him to replace the machine with a system that could compete in modern markets, but he insisted that his methods of investing were timeless and universal. The lifetime contract forced them to remain complacent. The world’s largest hedge fund was running on an Excel spreadsheet as recently as 2018.

In recent years, Bridgewater’s performance faltered, a result of both an unfavorable macro environment for Dalio’s thesis combined with increased competition from hedge funds with sharper trading algorithms.

The 10 year return on Bridgewater’s All Weather Fund (2014-2023) was 43%.

The 10 year return on a 60/40 stock-bond portfolio during that time was 90%.

All things considered, the lifetime track record for Bridgewater Associates is incredibly impressive when you consider their very limited number of down years, the ability to scale to a level that other hedge funds couldn’t, and the fact that all investing was done by Dalio and his inner circle.

But the other funds are catching up.

In the near future, a new victor will claim the once untouchable throne of the world’s largest hedge fund.

It’s worth taking a step back and thinking about the scalability of hedge funds as a business.

The difference between most hedge funds and their alternative investment sibling - private equity - is liquidity.

For hedge funds playing in liquid markets such as equities, currencies, fixed income, etc., their performance can be analyzed in short term intervals. A hedge fund with a few bad years is cooked. Investors are able to see performance in real time and request redemptions, which ultimately means withdrawing their money. Redemptions aren’t necessarily easy to come by - usually hedge funds will have a lock-up period ranging from six months to two years for new investors. But in comparison, private equity limited partners have no option to redeem capital. Once you invest in a certain fund, you’re simply waiting for returns over a long term horizon. In addition, most hedge funds stay within their strategy while most private equity funds scale to a certain AUM, then launch other strategies such as private credit, growth equity, real estate, etc., that bring in fresh funds.

Short term volatility, liquid markets, and competitive dynamics are some of the factors inhibiting hedge fund scalability. Imagine if NBA contracts were on a six month basis. This is the game that most hedge funds play.

The five largest hedge funds in the world manage anywhere from $70B - $100B.

The five largest private equity funds in the world manage anywhere from $400B - $1T.

But that’s a story for another chapter.