State of Venture

Thoughts on fund distributions over time. Detailed data on Sequoia, USV, IA Ventures, and Forerunner returns.

Starting a venture capital fund, in theory, appears to be a simple endeavor: raise money from investors, deploy the capital into elite early-stage companies, and return a multiple of that capital to the investors.

The lack of liquidity in private markets has been a loud talking point recently, so those who are able to do so will separate themselves from the pack and attract even more capital in the future.

Oftentimes, LPs become frustrated when it’s year six, seven, or eight, and they haven’t seen any meaningful capital returned.

Even more frustrating is when the paper returns through markups seems to portray that the fund is killing it, yet they have nothing to show for it.

This phenomenon perfectly represents the DPI (distributed to paid-in capital) versus TVPI (total value to paid-in capital) debate.

However, there are numerous examples of funds that have insignificant DPI figures for nearly the entirety of the fund life up until the very last moment.

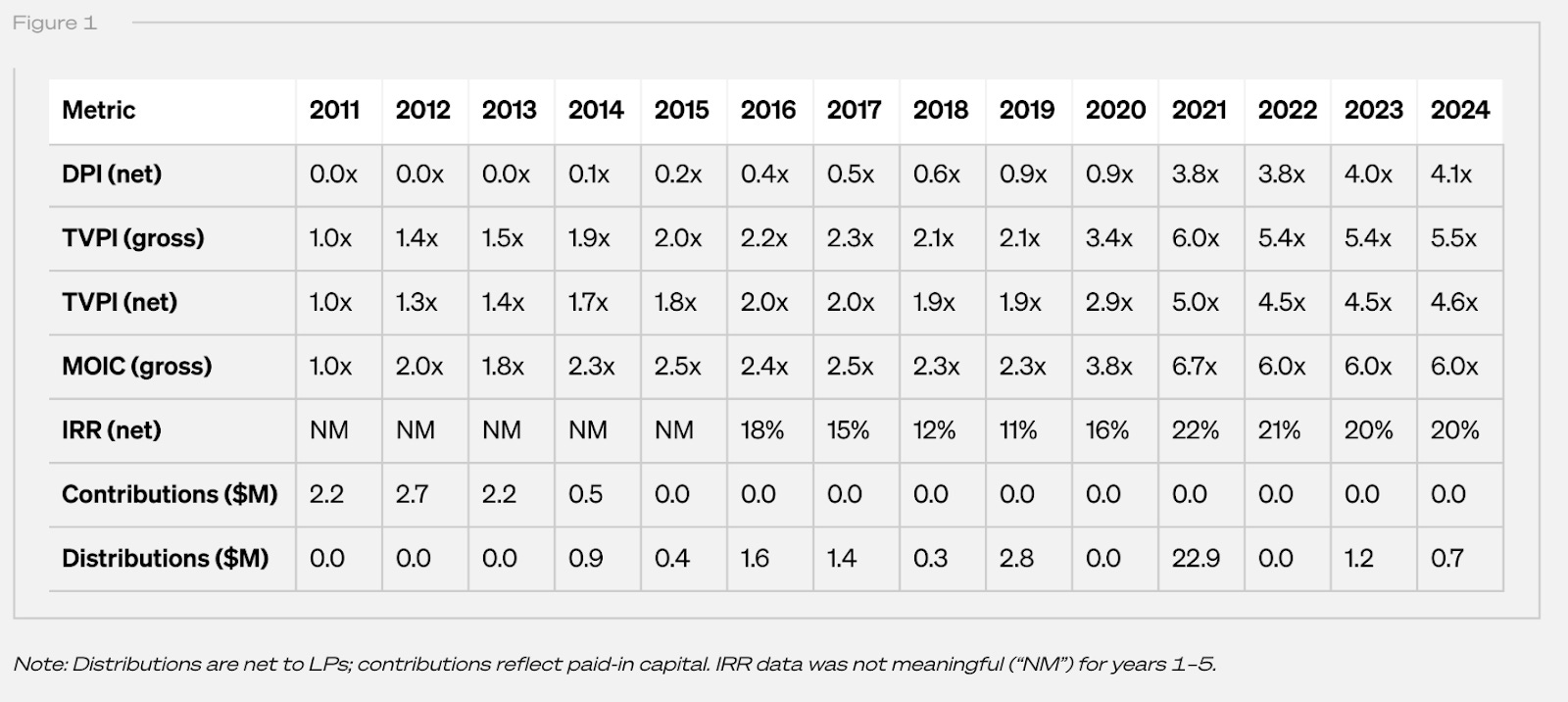

One example of this is Collaborative’s Fund I in 2011.

The fund was on the smaller side, investing $8M across 50 companies with check sizes ranging from $10K to $400K. They focused on pre-seed through Series A companies and were sector agnostic.

By year ten, while they had a solid net TVPI of 2.9x, their DPI - the metric LPs actually care about - was only 0.9x, meaning investors had recouped about 90% of their original investment.

Most fund lives are roughly ten years, so it wouldn’t be surprising if LPs had already written this fund off as mediocre.

Everything changed in year 11.

In the blink of an eye, net DPI soared to 3.8x, making it one of the top performing funds of that year.

For more context, PitchBook states that a 3x net DPI is roughly 90th percentile.

Interestingly enough, after 14 years, there is still a slight discrepancy between TVPI and DPI (4.6x versus 4.1x), placing the GPs in an interesting dilemma as to whether they want to ride it out or find that last chunk of liquidity for investors.

The importance of the power law for venture investors cannot be understated.

Eight companies - Upstart, Lyft, Scopely, Blue Bottle Coffee, Maker Studios, Gumroad, Reddit, and Kickstarter - drove nearly all distributions, contributing roughly 95% of all returns.

These eight companies represented $800K of invested capital but returned $37.6M - an astonishing 45x return.

The remaining 42 investments - $7.2M - returned a disappointing $2M.

Even more interesting is the power law within the power law.

Of those eight companies, only one of them delivered 73% of all capital returned to investors.

This perfectly represents venture ethos: swing for the fences every time because although you’ll strike out more times than not, all it takes is a one or two grand slams to get the job done.

The seemingly obvious takeaway from Collaborative’s Fund I is for LPs to prioritize patience because many times, the value being created over time may not be realized for a while.

But you could easily have a different take on this.

What if it really was an average fund that happened to benefit from the excess capital and abnormal levels of liquidity we saw in the venture ecosystem around 2021?

Sure, there is always some luck involved with startups and venture funds, but in the alternative timeline that 2021 was just another run-in-the-mill year for VC, there’s a high probability that this fund maintains the average metrics it had posted for the past decade.

Coming back to the actual timeline, 2021 was a massive year for VC and those with vintage funds around the early 2010s reaped the benefits.

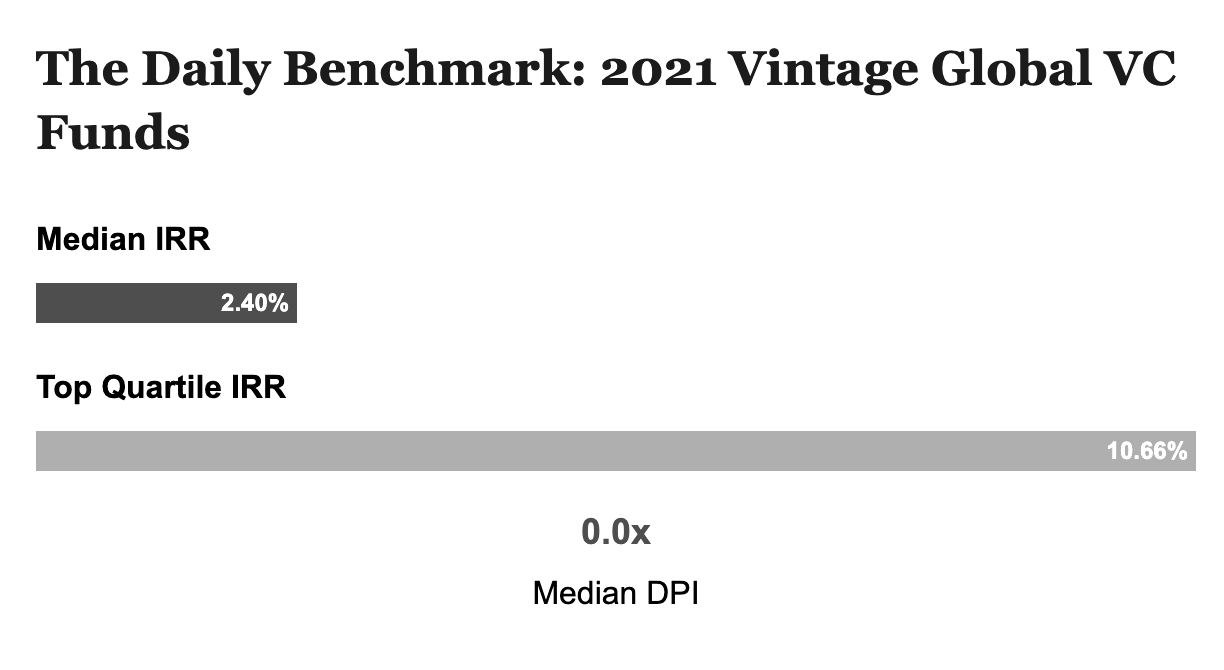

On the flip side, those with vintage funds close to 2021 have not had the same fortune, to say the least.

While a 0x median DPI makes sense given the short time frame, a median return of 2.4% IRR is unbecoming.

Timing is important in venture.

Earlier this month, we made a public records request to UTIMCO, the University of Texas endowment system, for their fund investments and returns. Here are some of our most interesting findings:

Union Square Ventures is elite.

UTIMCO invested a total of $129M across 7 different USV funds and average IRR across those funds was 59.2%, making it UTIMCO’s best venture investment when taking size, IRR, and DPI into consideration. Their 2012 vintage returned 22.9x cash on cash, giving UTIMCO $500M+ in distributions from a $25M investment. USV is a case study in remaining small - they refuse to raise funds larger than a few hundred million - while their competitors continually test the limits of venture fund size.

Sequoia hasn’t been too hot lately.

To be fair, these are relatively new vintages: Growth Fund IX = 2020, Venture Fund XVII = 2020, US/E Seed Fund IV = 2022. Probably would be better to check back in a few years before jumping to a conclusion; nonetheless, the amount of capital firms like Sequoia have been raising make it awfully difficult to generate top-decile venture returns.

IA Ventures is second only to USV.

Another testament to staying small. Fund I and II were both home-runs, while III underperformed with a 10.3% IRR and no distributions so far. Fund III was a $160M 2015 vintage. Even with that miss, IA Ventures has generated a 40.9% IRR on $140M invested by UTIMCO across 6 funds.

Forerunner is good at fundraising.

The performance here is a little better than what it seems considering Builders III (-13% IRR) was a 2021 vintage. The most interesting thing with Forerunner is how much they raised so quickly relative to other funds. I’m going to guess that their Fund II, which UTIMCO didn’t invest in, did very well. In 2022 they raised $1B across two funds, $500M for Builders and $500M for Partners.