Pro Populo

as organic as beyond meat

America was booming.

Specifically the population, as the country had just concluded a gruesome war that saw many of its soldiers sacrifice their lives.

But we are not referencing the frequently scapegoated baby boomers and WWII.

The scene is post Civil War.

Between 1860 and 1890, the country’s population more than doubled from 31 million to 63 million. This caused several notable effects, but the most pertinent was a drastic increase in food demand. Thus, many saw where the tides were shifting and set their sights on becoming farmers.

Since many of these prospective farmers–who were now journeying westward–calculated that the growth in demand for food would be stable in the short to mid term future, taking on debt from east coast banks seemed like the cheapest way to grow their economic prospects.

Things were going according to plan until they weren’t.

Global competition and overproduction led to falling crop prices, monopolized railroads began to hike transportation prices, and droughts rendered significant portions of farmers’ crop supply useless.

Farmers began going bankrupt left and right.

After seeking help from the government, specifically to regulate the railroads, the politicians yawned and told them to get lost because it wasn’t their problem. While sounding cliche, the farmers had no other option but to band together and advocate for themselves. They used the help of labor unions and worker organizations to expand their reach, creating The People’s Party in 1892.

American populism was born.

Over the years, it was used strategically by left wing figures like James B Weaver and Huey Long as well as right-wingers like Joseph McCarthy. After McCarthy, it hit a bit of a lull but it would soon resurrect.

“For too long, a small group in our nation’s capital has reaped the rewards of government while the people have borne the cost. Washington flourished—but the people did not share in its wealth. Politicians prospered—but the jobs left, and the factories closed. The establishment protected itself, but not the citizens of our country. Their victories have not been your victories; their triumphs have not been your triumphs. That all changes—starting right here, and right now, because this moment is your moment: it belongs to you.”

Donald Trump

“We are going to create an economy that works for all of us, not just the 1%… We will all come together to say loudly and clearly that the government of our great nation belongs to all of us, not just a few wealthy campaign contributors. That is what this campaign is about… that is what the political revolution is about.”

Bernie Sanders

Populism awoke from its slumber in the mid 2010s. Donald Trump quickly garnered a loyal fanbase by creating a clear bifurcation between the constant stream of corrupt politicians that enriched themselves at the expense of the people and himself, a political outsider that could theoretically not be puppeteered by outside lobbying influences due to his financial independence. On the other side of the political aisle, Bernie Sanders became popular among the youth with a similar yet distinct socialist outcry of the financial and political elite conspiring to keep the masses oppressed. Both Trump and Sanders benefitted from a relatively stagnant economy, growing popularity of social media platforms, and growing distrust of the Mitt Romneys and John Kerrys of the world.

More than a decade later and the populist bug is still in the air.

Some argue that it hasn’t left the political scene and both sides still await their true populist messiah.

But where it is undeniably present is in the private investing world.

In a surprising turn of events, many voices have begun to ask the question of “How do we increase retail investors’ access to private assets?”

But what if retail investor access isn’t actually the goal? More importantly, if the actual goal is simply to increase fund manager access to a new–and rather large–capital source rather than retail investors’ access to private funds, does that actually matter if access is gained nonetheless?

This move would only make sense if fundraising became noticeably more difficult in recent times.

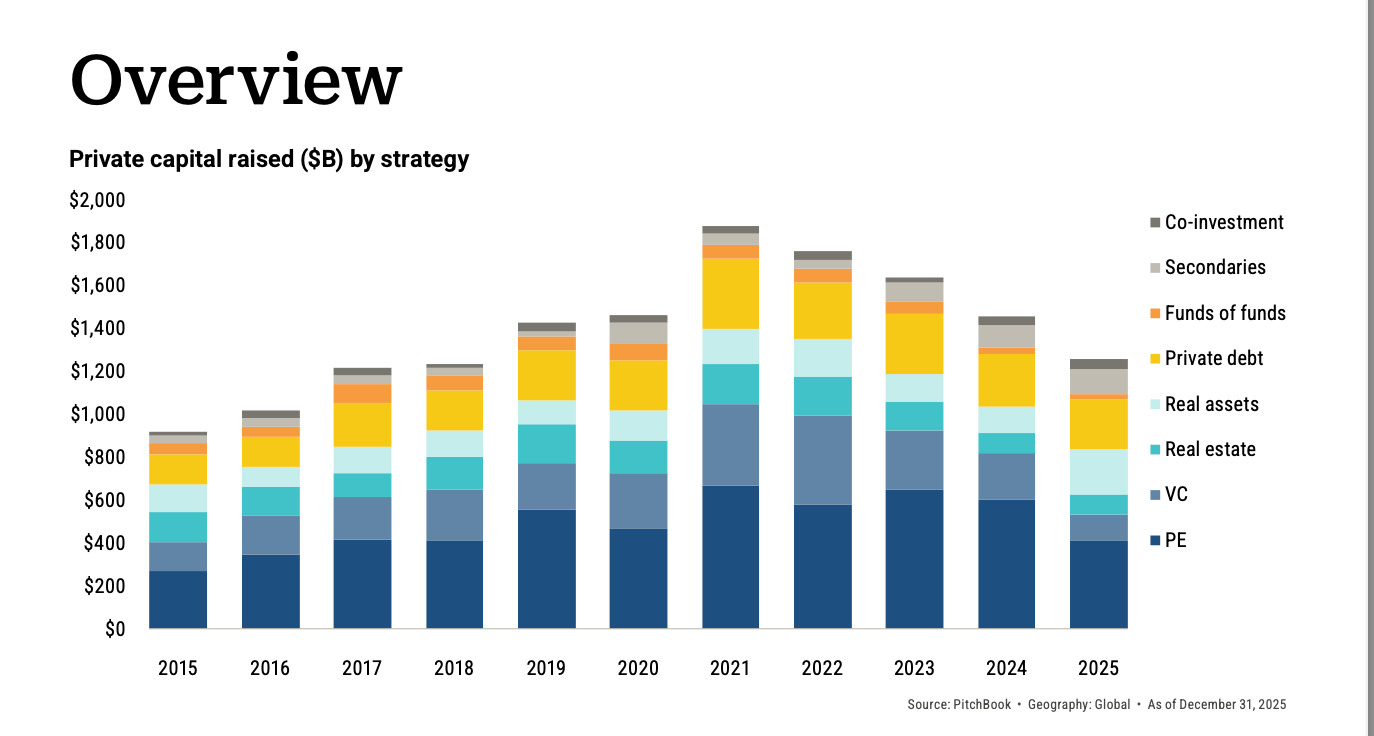

As the data shows, private capital raised across the board has seen a downward trend since the 2021 peak, with venture capital and private equity following the trend. Not only has the total amount raised between the two assets decreased, but their share of capital within the private ecosystem has decreased as well, as LPs have shifted to assets like infrastructure, secondaries, and private debt, given the lack of cash flow PE and VC has provided recently. PE specifically has seen fundraising decrease to $414.2B in 2025, a 38% decline from the 2021 peak. In VC, the biggest players increased their share of capital raised, as 22% of commitments were closed by 10 funds, the highest since 2012.

Thus, one cannot say that the executive order signed in 2025 aiming to expand access of 401Ks and other retirement plans to private assets was a coincidence. It doesn’t take a genius to realize why all of the loudest voices for democratization were nowhere to be found in 2021 when institutions were handing out cash like everyone’s favorite uncle on their birthday.

While no major shifts have occurred yet, regulators have been working overtime to figure out how to actually implement these changes while the biggest fund managers are curating specific products catered towards them.

While many of the biggest PE funds are gearing up for this shift, several of their friends up the capital stack tapped into the trend slightly before the noise became loud. Private credit funds like Blue Owl, Cliffwater, Apollo, and others have steadily allowed high net worth individuals to access their products through evergreen funds, mainly BDCs. These structures differ from the typical private funds in that they allow a limited % of assets to be redeemed per quarter, usually around 5%.

The dynamic between these HNWIs and the funds was unproblematic for a while until the murmurs about software companies’ vulnerabilities to the AI revolution became louder in recent weeks, with software stocks undergoing a noticeable correction. Most of these funds lended a decent chunk of their assets to software companies and some investors became spooked and decided to redeem the assets.

Similar to your average bank, these semi-liquid structures are only functional when a relatively small portion of investors redeem their cash at the same time, as nearly all of the original capital has typically been deployed to the companies. Thus, the funds will typically draw from either new LP cash, their relatively small portion of funds held in cash or its equivalents, or through credit facilities with the underlying loans serving as collateral.

As the demand for withdrawals has surged far past the traditional 5% limit, these funds are faced with a decision: either increase investor confidence through granting requests or protect themselves and prevent all of the requests from being granted. While the first option seems like the “right” thing to do, many of the firms would likely have to increase their leverage exposure.

Blue Owl has taken the safer path, limiting redemptions in one of its most notable funds, although they were able to satisfy some requests through selling a third of the fund’s assets for 99.7 cents on the dollar. While coming that close to par was likely a best case scenario, many in the industry are still nervous about the portion of the fund’s assets that needed to be sold.

Cliffwater and Morgan Stanley also limited their withdrawal requests as well, with both funds exceeding the typical 5% but not accepting all requests. One of Cliffwater’s funds–holding $7.6B in assets–saw withdrawal requests shoot to 14%, in which they honored about half of them. Morgan Stanley’s situation was similar, fulfilling about 46% of the 10.9% request figure.

The problem with these types of structures became obvious. Firstly, they are more opaque than many investors realize, as not only do the investors redeem shares at NAVs that are determined by the fund managers that can inaccurately price these assets that rarely trade, but many evergreen funds buy secondary interest in other managers’ drawdown funds, creating a fund-of-fund type structure that many investors aren’t aware of. For instance, Blackstone’s new hedge funds for “mini-millionaires” will have roughly a third of the fund’s assets invested in other hedge funds, creating a less than ideal double fee structure.

When good times abound, most don’t pay attention to these types of issues.

But it’s a different ball game when things turn downwards.

When the market deteriorates, while fund managers have to worry about the value of their assets decreasing, they typically don’t have to worry about all of their investors rushing to their door, demanding they get their money back, as the institutional investors that back these funds know they signed up for the long time horizon that will ideally be rewarded through increased returns. However, as the share of capital through these semi-liquid evergreen funds increases, in downturns, managers will not only have to deal with declining NAVs but also a flood of withdrawal requests that will likely not be feasible. The system has already shown vulnerability based on weakness in a specific industry, so only time will tell what happens when the broader macro environment is hit with a negative shock. We’ve seen a spike in requests simply based on fears of future software performance, and the fact that most of the underlying loans themselves in these major funds are healthy seems to be irrelevant to the sentiment.

While the bears have been predicting a recession since late 2022, many economists have an active eye on the macro conditions, especially with the low consumer sentiment due to increased gas prices from the Iranian conflict.

In addition to the apparent gap in the armor, many have been discussing the paradox of increasing private assets access to the masses. Specifically when analyzing the relationship between public and private equity, as more investors gain access to private equity through structures that provide some sort of periodic liquidity, private equity begins to look more like public equities, as the lack of liquidity is one of the key features of private equity. Additionally, as the retail capital floods the private scene, there is an increased likelihood that it may lead to bidding up the entry prices, thus competing away the excess return that private equity–in theory–provides relative to its public counterpart. The entry price is obviously one of the key metrics when determining rates of returns and the inverse relationship between return and purchase price could potentially eliminate the attractiveness of private equity. This is highly theoretical, and the practical doesn’t always fall in line with the theoretical, but it is nonetheless something to keep an eye on.

Thus, the verdict of whether retail investors should access private assets en masse, and if so how, becomes unclear. Access of some sort seems inevitable at this point, but the real mystery lies in how to create a mechanism that will provide access without creating potential headaches for both the investors and managers.

What is perfectly clear, however, is that the push for retail investor access to private markets was not an organic populist movement but rather the titans looking for their next meal while saving some crumbs for the masses. In a strange way, there could be a scenario in which both parties are satisfied given that crumbs are better than the empty plate they had before. Where it could get dangerous is when the people realize the crumbs they were given were not as they originally appeared, as a revolt is inevitable once they realize it wasn’t real food to begin with but rather synthetic, lab-grown food.