ATOMIC.

abraham's idea factory.

Today’s memo is brought to you by Caplight.

Caplight puts VC data and deal flow in one place.

The best venture investors in the world use Caplight to track private company valuations and fundraising activity, and to trade the private markets.

Book a demo here.

There’s a lot in a name.

Technically speaking, Anthony Edwards, Draymond Green, and Domantas Sabonis are all “basketball players.” To someone who does not watch basketball, the assumption is that these three players do similar things for a living. That assumption, as basketball viewers know, is absolutely false. Anthony Edwards gets paid to score from all three levels - near the rim, the mid-range, and the three pointer - and occasionally jump over unsuspecting opponents like an NFL athlete.

Draymond Green gets paid to anchor the defense, frustrate the other team’s best player, and orchestrate the offense. His mind and attention to high level game strategy are arguably more important than his physical tools. Domantas Sabonis is paid to get a double-double every night by using his size advantage to finish around the rim, grab rebounds, and create offensive advantages as a screen setter in pick and roll actions. Anthony Edwards, Draymond Green, and Domantas Sabonis are all basketball players, but they do very different things for a living. This is why positions were created to better describe roles. Anthony Edwards is a shooting guard, Draymond Green is a forward, Domantas Sabonis is a center. As the game got more complex and “position-less”, more creative ways to precisely label players began to emerge. Rashad Phillips is a Detroit Mercy Hall of Famer for his basketball career there; at just 5’9, he was one of the leading scorers in school history with 2,319 career points. He played a year in the NBA’s Developmental League before embarking on a ten year overseas journey across Germany, Turkey, Greece, and Saudi Arabia. He retired in 2010, but recently found a new lane doing scout analysis as an independent outlet under the Twitter handle @RP3Natural. One of his major contributions is re-defining traditional positions, which he does in his book, Basketball Position Metric: The Evolution Is Being Televised. Instead of point guards, shooting guards, small forwards, power forwards, and centers, Phillips introduces a much wider slate of options to label more complex players: traditional guard, point guard, hybrid guard, combo guard, shooting guard, small forward, dual forward, stretch big, hybrid post, power forward, center, and point center. Lebron is a dual forward, Chris Paul is a point guard, Steph Curry is a hybrid guard, Karl Anthony Towns is a stretch big. Over time, the way analysts label and evaluate players becomes increasingly specific in order to accurately assess different skillsets.

A similar evolution is silently taking shape in venture capital. Limited partners and founders are starting to wake up to the different forms of venture capital outside of traditional investing parameters. For instance, accelerators are not the same as pre-seed investors, even though they invest in startups at similar stages. And some of the general partners running alternative strategies are sick of being labeled as “venture capital funds”.

Jack Abraham is one of those general partners.

The serial founder launched Atomic VC in 2012 with $10M of his own capital.

The outfit most recently raised $320M for its fourth fund in 2023.

In a Harvard Business School article, Atomic VC partner Chester Ng rejects the idea that Atomic is a venture fund: “We’re definitely not a venture capital firm… We’re not an accelerator or incubator either.”

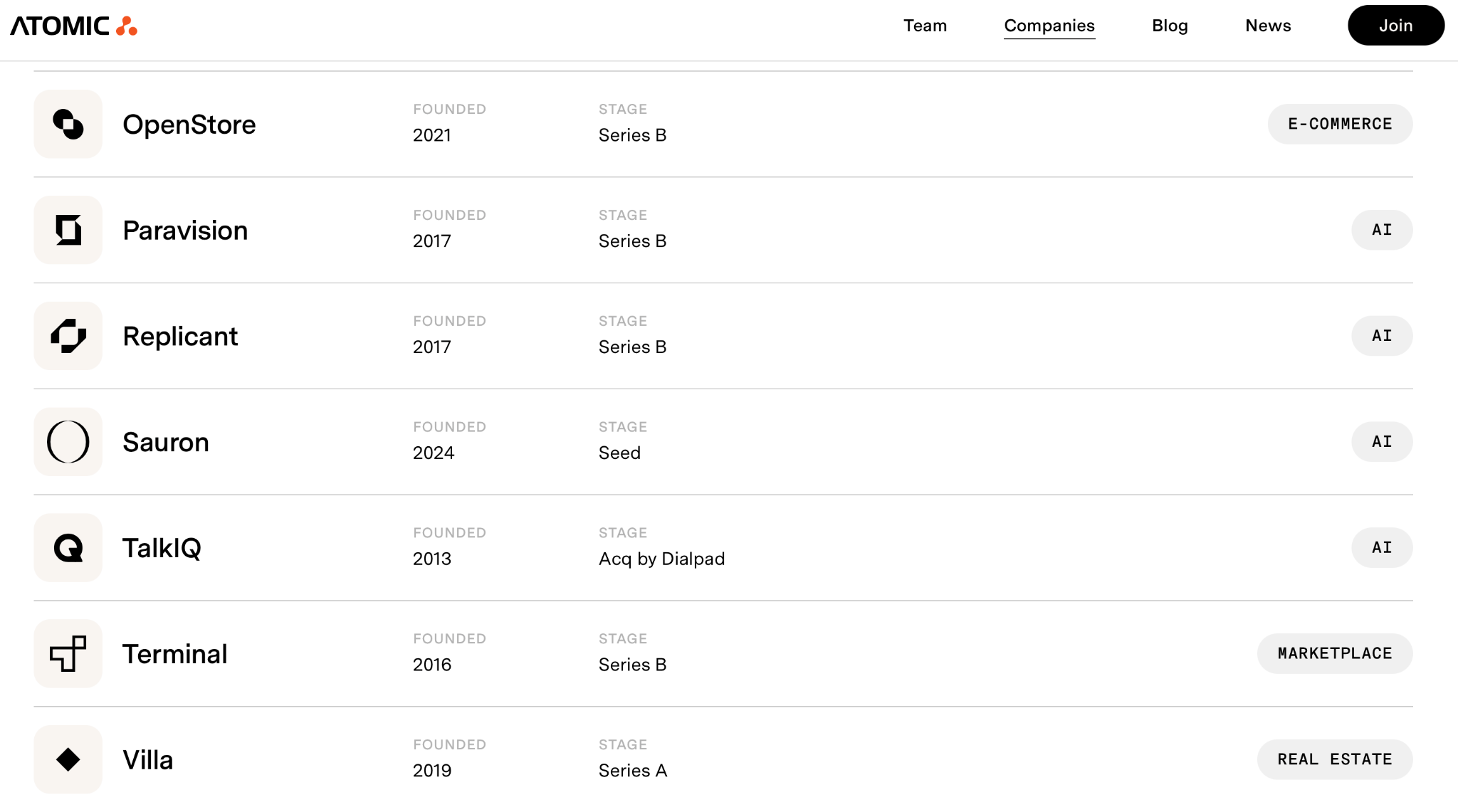

There isn’t much you can find online about Atomic.

You can search for their fund announcements and Techcrunch will tell you how much they raised recently. Or you can look up their team roster and see that Jack Abraham is the founder and CEO, Chester Ng is a general partner, and Kristin Schaefer, a former Postmates CFO, is their most recent general partner hire. You can even go on their website and look at a couple of companies that they’ve invested in - or, more appropriately, built, or even more specifically, conceptualized… perhaps there’s no word in the English language to precisely describe what Atomic does. But if you put your reading glasses on, you’ll quickly realize that the companies listed on Atomic’s site are outdated; the fund only lists companies they’ve backed in the past that were successful. 15 out of the 17 companies listed were founded between 2012 and 2021, and the two other companies were founded in 2024.

You would also struggle mightily to find data on fund level returns: Atomic has done a great job of barricading public limited partners - U.S. public pension funds or public university endowments - from investing in their vehicles, because public LPs are required to disclose fund level data to the public, so if Atomic had public LPs, the data on their fund returns would be available to anyone. Instead, Atomic’s LPs include the most famous venture capitalists in the world, such as Peter Thiel and Marc Andreessen, and institutional investing firms like Stepstone Group ($149B+ AUM), with the latter accounting for 90% of the fund’s capital.

To cap it off, Atomic operates out of Miami, Florida, a detail that initially seemed insignificant until placed next to other pieces of damning evidence on the conspiracy board. Upon further examination, it seems as if Jack Abraham tried to run as far away from San Francisco as possible, with the hope of evading any undercover agents that could erode the information advantage his fund has. A firm this focused doesn’t move to Miami for the weather.

We were very annoyed in the last cycle where we would start companies and there were literally other studios that would send spies into our studio.

Jack Abraham, Atomic founder, to Auren Hoffman

Secrecy shrouds Atomic like a mushroom cloud; it is the Manhattan Project for startups.

Magid Abraham was born in 1958 and raised on a fruit farm in Machghara, Lebanon. The town’s name roughly translates to “strong and abundant flow of water,” a reference to the springs that power Machghara’s agricultural economy. Nearly 30% of Machghara is agricultural land, and the main crops are fruit - apples, grapes, pears, and cherries - so Magid’s upbringing on a farm was common. At a young age, Magid’s father taught him that it was better to own something than to work for someone else. Magid’s father owned multiple fruit orchards and spent days working hours in the sun, doing manual labor. It was a small town at the time, and still is today; no more than roughly 9,000 people live in Machghara on a full-time basis.

At the ripe age of thirteen, Magid moved from Machghara to one of the largest cities in the Middle East. He went to Beirut by himself, searching for the best high school education in Lebanon. His journey as a scholar was one of consistent excellence. After grinding his way to the top of his class as a teenager in Beirut, he traveled to École polytechnique, the top engineering school in France, where he excelled and then moved on to a MBA and PhD from MIT. While studying at MIT, he slept on a concrete floor in a sleeping bag. Magid was a relentless learner… In 1985, he joined Information Resources, Inc (IRI), a data analytics company that delivered market research on consumer shopping patterns to corporate clients. Just a year after joining IRI, Magid and his wife Linda welcomed their first child to the world. They named him Jack. In 1995, ten years after initially joining IRI and nine years after Jack was born, Magid and Linda founded Paragren Technologies, a marketing automation software company, which was later acquired by Siebel Systems in 2000, and Siebel was later acquired by Oracle in 2006. In 1999, Magid co-founded ComScore, a market intelligence company that he eventually took public in 2007. ComScore’s valuation on the first day of trading was around $640M and it hit a peak valuation of $1.6B in early 2016. Magid’s trophy room includes a “40 under 40” award from Crain’s Chicago Business, a “Technology Pioneer” award from the World Economic Forum, “Entrepreneurship Hall of Fame” induction from Ernst & Young, and the “Buck Weaver Award” from MIT Sloan School of Business. Magid’s life story is an American Dream case study. The son of Lebanese fruit farmers traveled thousands of miles across the world and found wealth beyond his wildest fantasies. If Magid Abraham’s life was a movie, Jack Abraham had the best seat in the house.

At the ripe age of thirteen, Jack started working nearly full-time at ComScore alongside his father. He was working with college graduates and other people twice his age, learning valuable skills such as programming and data visualization. The confidence Jack developed from having a seat at the table allowed him to constantly live outside of the box. Even as a high school student, he came up with his own changes to the processes his dad let him run.

Jack also got early exposure to the volatility of managing a startup company. During the summer of 2002, Magid, Linda, and Jack took a vacation to Outer Banks, a chain of barrier islands off the coast of North Carolina, now known for the Netflix series named after the region. Magid was the furthest thing from relaxed; even a young Jack could sense his angst, but his father would not tell him what the problem was. Unbeknownst to the kid, Magid’s company had two weeks of cash left in the bank and he was frantically dialing the phone to find new investors. The market for funding startups was drier than Machghara in July. The dot-com bubble was still fresh in the psyche of technology investors, and Magid was facing a near death experience. ComScore ended up surviving, but the experience of seeing just how sticky things can get stuck with Jack forever.

In 2004, Jack started college at Wharton.

He didn’t graduate.

In 2007, he dropped out to start a local product search engine company called Milo.com.

Today, it’s easy to gloss over the last sentence. Dropping out of college to start companies has been normalized, even championed in many circles. Programs like Thiel Fellows and Y-Combinator have created pathways for elite students to take a break from their academic lives and see if they can build a revenue generating company. If not, they simply return to their ivy-coated campuses, finish their degrees, then either try again or get a job at Ramp. But dropping out of a college like Wharton in 2007 to start an unproven company was extremely rare and high risk. The only ones dropping out were the ones who couldn’t see themselves doing anything else - they were willing to die to be a founder.

Milo.com was a site that enabled shoppers to research online with the purpose of buying local. It gave users real-time inventory and availability information for local products, basically bringing an Amazon feel to supporting nearby retailers. Jack was living in an apartment on University Avenue in Palo Alto, and he was introduced to high-profile founders like Jawed Karim (YouTube co-founder) and Keith Rabois (Slide founder, venture capitalist), who helped him focus his value proposition. Milo launched in 2008 and site traffic grew roughly 70% month-over-month, going from roughly 2,000 visitors per month to over 1,000,000 in a year.

Milo.com was acquired by eBay in 2010 for a reported $75M.

At just 24 years old, Jack was a young prodigy at eBay. It was in the midst of this transition, from the frenetic pace of startups to a more stiff corporate environment, that Jack’s mind began to linger to another world. He had heard too many stories of his founder friends who get acquired, join a larger company, and become vegetables, mere shells of their former selves without any guiding motive in life. He decided that would not be his story.

Jack started doing whatever he wanted to do at eBay; he had an epiphany and realized the worst case scenario is he would get fired, which was not a terrible thing in his book. At the peak of the madness, Jack riled up his co-workers Boston Tea Party style and convinced everyone that cubicles were holding them back from their fullest potential, and in a matter of minutes, eBay employees were ripping cubicles out and throwing them on the front lawn at eBay’s San Jose campus. No one was fired.

The pranks were just a way of passing time. Jack’s mind kept coming back to building new products. He dreamt of a world where he could ideate on multiple concepts at once, have teams of engineers and product managers build them out, and steer these numerous ships with ease, like a teenager dominating his friends in Call of Duty, ejecting the disk, inserting Madden, and dominating them some more without losing a single iota of focus. Jack dreamt of a world with no constraints to building new things, where he could seamlessly deploy human capital to create new solutions to expensive problems and he could deploy financial capital to double down on things that are working. Money wasn’t real.

He pitched the CEO of eBay at the time, John Donahue, to let him build out multiple products using different teams. The results were almost all positive: Jack and his teams built products that translated to real revenue and brought good press to the company, consequently driving up stock prices. In one episode, Jack convinced Donahue to let him fly out six eBay employees to Sydney, Australia, rent an Airbnb, turn it into a hacker house, and build a product for two weeks straight. The resulting product became the feed and homepage for eBay, which became the primary discovery mechanism for the 130 million people using the site.

What I remember about Jack was that very early on he was very enterprising. When he was 3 years old he would go and talk to his friends, and he would convince them to exchange an old quarter for a shiny nickel… He went to a national marketing competition [in high school], and he was a finalist. He realized he needed to have a jacket, and he didn’t have time to go back to his hotel. So he convinced a total stranger to part with his jacket [and won]. He showed confidence, chutzpah, salesmanship.

Magid Abraham to Forbes

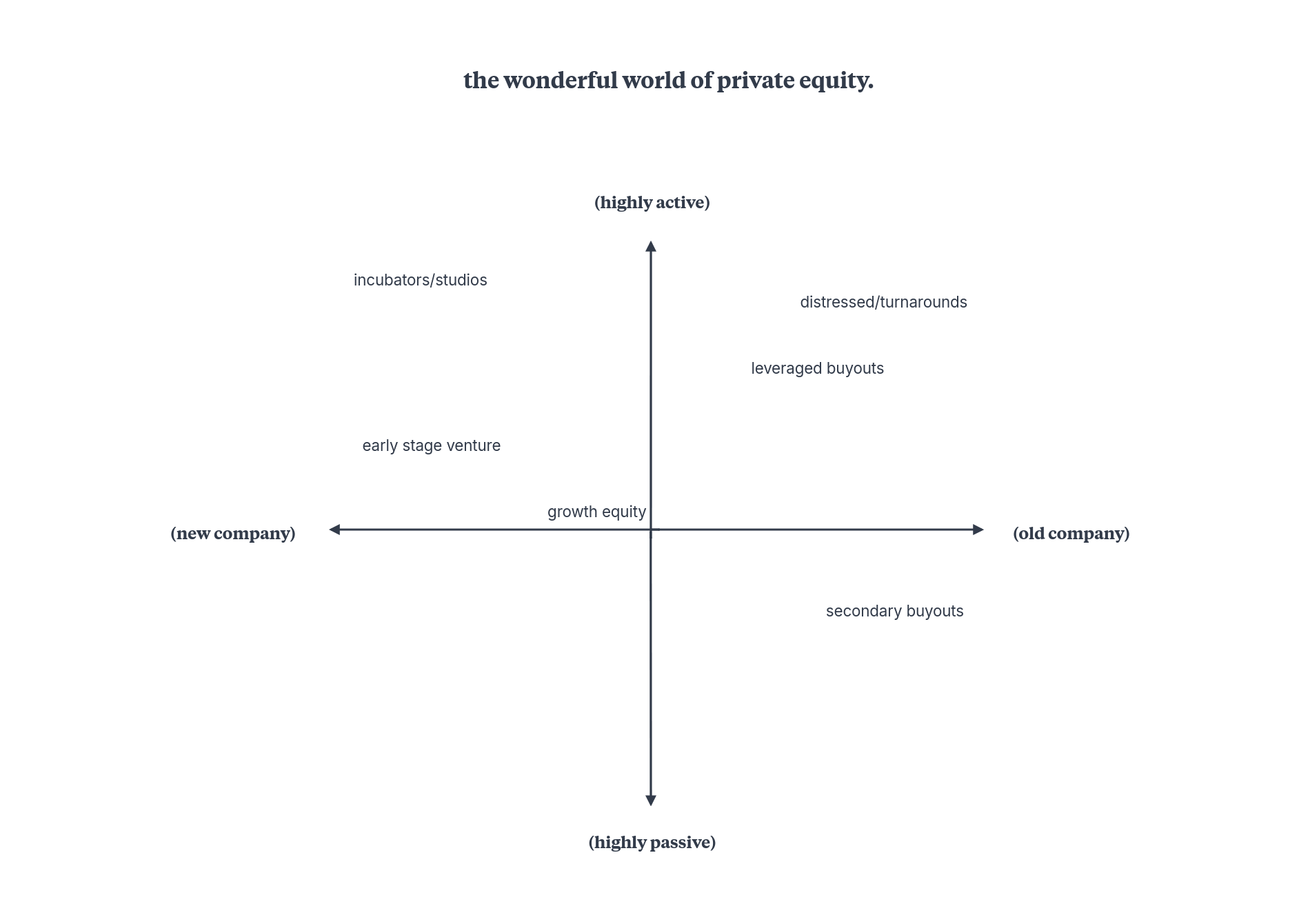

Private equity, as a word, is typically used to describe leveraged buyouts, a transaction in which a leveraged buyout fund acquires a controlling stake in a relatively mature company using a mix of debt (leverage) and equity (cash), with the goal of improving operations and financial structure before selling the company to a new buyer or taking it public and getting a return on initial capital. The inclusion of debt amplifies the cash return, making the transaction more lucrative than a simple “buyout.” When you hear about private equity in the mainstream media, pundits are almost exclusively talking about leveraged buyout firms like KKR, Blackstone, and Apollo. But private equity linguistically includes a wider range of strategies, such as growth equity, distressed private equity, and venture capital. Private equity technically includes any private stock financing, not just leveraged buyouts.

While leveraged buyouts get all the “private equity” media attention, early stage venture and growth equity get all the “venture capital” media attention, and less covered strategies such as incubators, distressed private equity, and secondary buyouts sit in the shadows of their famous family members. Everyone knows Stephen Schwarzmann from Blackstone, Henry Kravis from KKR, Josh Harris from Apollo, Orlando Bravo from Thoma Bravo. Likewise, Marc Andreessen and Peter Thiel have become household names. But the average business savvy American cannot name a single high profile investor who founded a venture studio, distressed private equity firm, or secondary buyout firm. There are a few ways to explain why there’s a lack of attention on these lesser known private equity sub-sectors.

The sheer deal volume and transaction size for the leveraged buyout industry makes it low hanging fruit for media outlets. It’s easy to write an article whining about the risk leveraged buyout funds pose to the American economy and use Schwarzmann’s latest $21B buyout fund as a data point to drive the point home. Everyone wants to talk about how these decabillionaires amassed so much wealth through financial engineering, and private equity moguls are happy to make the rounds on CNBC, Bloomberg, WSJ. Venture capitalists are famous due to their involvement in defining technology companies. Peter Thiel invested in Facebook, Palantir, Stripe, LinkedIn, Spotify - all companies that create products used by countless everyday Americans, businesses, and in Palantir’s case, governments. Shiny objects attract eyeballs, eyeballs drive the media cycle, and venture capitalists pay people to build more shiny objects. There are also few stories as powerful as the story of a few people going from nothing to something. From students in a college dorm room to a trillion dollar public company. From a quiet startup in Sweden to displacing the entire music industry. From two young Irish villagers to processing trillions of dollars in global payments. The startup story captures the human heart, and the heart controls the mind, and the mind directs media consumption.

Distressed private equity is far too technical to capture the heart of the average individual. In practice, distressed investing is an academic pursuit that legalistic financiers celebrate in their designated corners. Only a few skilled directors can take a distressed deal and come back with a Disney movie. Secondary buyouts are even further removed from winning hearts; at least with distressed deals, there is still tantalizing upside to be earned through savvy maneuvers and sharp litigation tactics; secondary buyouts are lifeless transactions, leveraged buyouts’ boring big brother that no one wants to hang out with. Telling someone you work at HarbourVest Partners will not ring a single bell, unless the person you’re talking to works at Lexington.

Risk and returns generally tend to increase when moving from highly passive investing to highly active investing, and from old, mature companies to new, unproven companies. So a pre-seed investor (new companies, very active) should have a higher risk/return profile than a secondary buyout investor (old companies, fairly passive).

What does this have to do with Jack Abraham?

In 2013, after ruffling feathers and shipping products at eBay, Jack Abraham had compiled enough business ideas to last a lifetime. During his commutes from San Francisco to San Jose, he would allow his mind to run wild with possibilities. When he left, there were more than two hundred and fifty ideas in his vault. At least one hundred of them were very good ones. He wanted to act on all of them, in a twisted mad scientist kind of way. He wanted to do what he couldn’t do at eBay. This is how Atomic came to be.

Atomic is a venture studio that takes ideas from concept to revenue, and then spins their companies out to raise additional capital from venture firms.

They do this by testing out ideas on their idea list, and then spending money, usually in the hundreds of thousands of dollars, to validate the ideas with end customers. When they get confirmation that an idea solves a painful problem for customers, they invest some more money, up to a few million, to go to market and generate revenue. At this point, when the company is running on its own and needs a larger check to accelerate growth, Atomic spins the company out of its studio and the company raises money from other venture capitalists. If the company is successful - let’s say an IPO - it works in Atomic’s favor because their ownership percentage is extremely high at the beginning, so even with dilution over time, a smaller outcome is still significant relative to capital invested. The fund math is more favorable from the ownership perspective, but on the other hand, the studio is time-intensive and typically has less portfolio companies than a venture fund, which is good for IRR metrics but usually results in a lower cash-on-cash return since exits are harder to come by with less shots taken.

Venture studios have one of the highest risk/return profiles within private equity and the opportunity set is dwarfed by traditional venture capital. Investors don’t build as many venture studios because (a) it requires a rather unique skillset and (b) there is no clear path to $5B+ AUM. If you follow the numbers, though, there has been a quiet uptick in the amount of capital flowing to studio platforms.

Andrew Dudum was born in 1988 and raised by Palestinian American parents in San Francisco. His primary ambition as a child was to become a rockstar and play guitar in a Billboard charting band. His mother, an astute woman, convinced him that in order to master the guitar, he must start with the fundamentals and learn the cello first, then in a few years, the transition would be seamless. Andrew ended up being an elite cellist and never touched the guitar nor a rock band. Instead of rocking the stage with Van Halen he toured the country with Villa Sinfonia, an orchestra that played at the Carnegie Hall, private concerts, and occasionally, weddings.

Andrew’s music resume helped open the door to arguably the most coveted undergraduate business education in America, Wharton. You can probably connect the dots here now - Andrew Dudum met Jack Abraham at Wharton. Like Jack, Andrew dropped out of Wharton to work on a startup. TokBox was a Sequoia Capital backed company that enabled business conference video chats, and it was acquired in 2012 by Telefónica.

In 2013, Andrew joined Jack at Atomic.

They raised $20M for its first fund, with a significant chunk coming from Jack’s earnings on Milo’s sale to eBay.

In addition to Jack and Andrew, there were two other partners. Chester Ng previously founded an app development company called SweetLabs and Andrew Salamon previously worked for Bridgewater Associates. The studio was located in San Francisco’s Presidio Park at the time, not too far away from Peter Thiel’s Founders Fund office (Thiel was an early investor in Atomic). The model was as follows: either start a company using one of the several hundred ideas the team had on a list, or partner with an intriguing founder to bring the founder’s vision to life.

In 2016, Andrew Dudum had an idea.

Epiphanies come in many forms, but a specific kind of epiphany takes place when an individual independently realizes that the textbook is wrong. Certain assumptions made on a societal level are not true, and when an individual realizes this, there is a sense of enlightenment; a similar feeling to uncovering a long lost secret or finding hidden treasure in your backyard.

Andrew Dudum knew there was an extraordinary opportunity to improve on the healthcare model. In a world where Amazon delivers same day packages, the traditional timesuck of a doctor’s visit didn’t make any sense. The issue is, healthcare has a ton of inefficiencies for a reason; regulatory constraints make the sector a graveyard for overly optimistic founders. There are general partners at Tier-1 venture firms who have sworn off investing in healthcare startups entirely. So Andrew took some time before taking any action. He decided what to build only after the vision became clear as day.

Andrew’s core realization was that healthcare is failing men for a few reasons:

Culturally, men do not seek out medical help unless there’s an emergency, which translates to worse healthcare outcomes for the demographic as a whole

Stigmas around certain health issues further perpetuate this cycle

Men actually do care about their health, but the inconvenience and stigma of dealing with it prevent treatment

Andrew figured if he could come up with a way to (a) de-stigmatize getting treatment for issues like baldness and prostate health and (b) make the treatment products desirable, then Atomic could build a generational healthcare brand from this wedge.

In 2017, Atomic launched Hims, and the brand did $1M of sales in the first week.

The brand did generational numbers in record time, raising $200M in venture funding from Thrive, 8VC, and Founders Fund.

Revenue scaled from $0 to $100M+ in less than three years.

2018: $26.7M

2019: $82.6M

2020: $148.8M

Profitability also improved drastically from 2019 to 2020.

2018: -$75.8M (loss)

2019: -$72M (loss)

2020: -$18.1M (loss)

It’s easy to gloss over the simply incredible growth trajectory that Hims hit in such a short amount of time, but I refuse to do so. In hindsight, the company is one of the top five fastest growing consumer brands of our time and probably the most underrated venture backed company considering both the explosive growth and longevity.

Hims & Hers ended up going public in 2021, just four years after initial launch. You would be hard pressed to find another company in the past ten years that graduated from private markets faster than a Wharton student graduates from undergrad. This is, to be clear, a record time, according to Atomic VC’s website. Incredible stuff.

Hims & Hers Founding Date: November 2017

IPO: January 2021 (via SPAC)

Time to IPO: 3 years, 2 months

Valuation at IPO: $1.6B

The sprint from incubation to IPO is impressive on its own, however, while I was reviewing the IPO S-1 filings, I found another gold nugget that adds to Atomic’s legend.

Oaktree, the renowned asset management firm led by Howard Marks, took Hims & Hers public via a SPAC in 2021.

If you are familiar with Howard Marks, you can feel the shock value in that statement. Marks is an exceptionally conservative investor that primarily made its money in credit - distressed debt, high yield loans, and private credit. Marks is nearly synonymous with taking intelligent risks, sitting out on easy money booms, and aiming for 15%+ IRR year over year. So why was he taking a venture backed startup public via SPAC in 2021? I thought this was Chamath Palihapitiya’s lane?

This reminds me of a conversation I had a few months ago with a friend. We were talking about the Warriors - Cavaliers rivalry from back in the day, and the topic eventually rested on the Game 7 when the Cavs miraculously beat the 73-9 Warriors team in what was one of the best basketball games of recent times. At one point during this discussion, my friend mentioned that Draymond led the Warriors in scoring that game. I responded as any rational person would, and said, no, that’s not true, let’s not make things up. I clearly remember Lebron pinning Iguodala’s layup off the backboard. I remember Kyrie’s shot over Steph Curry. I remember it was a gritty low scoring affair where every point mattered. But I couldn’t remember Draymond scoring 32 points.

Turns out he did; and not just 32 points, but 6 for 8 on three pointers, 11 for 15 on field goals, 15 rebounds, and 9 assists, nearing a 30-point triple double while shooting 75% from 3, 73% from the field, and just two turnovers, in Game 7 of the finals. When no one else could score, he provided more points, rebounds, and assists than Steph Curry and Klay Thompson combined. Draymond isn’t known to be a scorer, 32 points is the second highest scoring performance of his career, his career average is just shy of 9 points per game; he also isn’t known to shoot the three, he’s a solid 32% shooter on moderate volume (2.7). But in the biggest playoff game of the past ten years, he played like a completely different player - a flatout superstar. And I completely forgot.

From 2019 to 2023, Howard Marks and Oaktree were uncharacteristically active in the SPAC market, launching three SPACs - Oaktree Acquisition Corp, Oaktree Acquisition Corp II, and Oaktree Acquisition Corp III Life Sciences - while investing in a few others. The results are hard to detangle given the low sample size - Oaktree III Life Sciences pulled out of the market before acquiring a company - but if you take an average of the two primary vehicles, things are looking solid due to Hims & Hers strong stock performance.

Atomic is one of the few studios that can boast of successfully taking a company from incubation to IPO. The Hims & Hers exit returned 150x+ to the fund; as a result, the aggregate portfolio returns have been rock solid. In 2017, pre-Hims & Hers, Jack said Atomic’s IRR was at 65%, and in 2018, Atomic partner Chester Ng said their Fund I had a 70% IRR. Not much detail has been revealed since then.

Fund sizes have grown accordingly - from the initial $20M fund to a $150M Fund II to a $260M Fund III and most recently a $320M Fund IV.

As mentioned in the beginning of this breakdown, it’s difficult to decipher what Jack Abraham and the guys are building now. They’ve intentionally kept things stealth, treating each startup incubation as a military grade project unfit for the public’s eyes. The most recent unveiling is from 2024: Exowatt is a company that builds modular, dispatchable energy systems that capture solar energy, store it as heat, and use it to meet demands of AI infrastructure. A much more technically gritty endeavor than selling hair loss supplements, but I guess that just goes to show the range with which Atomic operates. After initial funding from Atomic, Exowatt raised a $20M seed round from a16z, Sam Altman, and Leonardo DiCaprio in 2024, then closed on a $70M Series A led by Felicis in April 2025, before raising another $50M from MVP Ventures and 8090 Industries in November 2025, for a total of $140M in two years. Energy efficiency for AI infrastructure is a massive problem for some of the deepest pocketed tech companies of all time, and by extension, a massive market to go after.

On the topic of AI, there is arguably no better time to own a venture studio. The biggest drawback of the studio model, according to multiple venture capitalists who have incubated companies, is the time cost. Instead of sitting and waiting for the right opportunity, reviewing tons of pitches and then allocating capital to the highest growth opportunities, the incubation model lifestyle looks much more like a professional early stage founder than an investor. Days are filled with customer meetings, user research, pitching investors to buy in at the seed stage, and other time intensive tasks usually reserved for people building companies. Of course, another executive is brought in to lead these tasks, but the investor’s typical routine is disrupted nonetheless, and there is a question of whether incubating while actively investing full-time is desirable, or even sustainable for optimal returns. With artificial intelligence, studios are able to iterate faster, test things quicker, and start more companies.

Since Atomic launched in 2013, the venture studio model has blown up.

From 2015 to 2025, the number of venture studios grew 15x+, from around 65 studios to over 1,000.

From 2022 to 2025, the number of venture studios as a percentage of new venture funds grew fourfold, from 3% to 13%.

Copycats began to flood the scene, and Jack Abraham moved to Miami to avoid them.

Who can truly tell us where ideas come from.

Ideas are like rabbits. You get a couple and learn how to handle them, and pretty soon you have a dozen.

John Steinbeck

New scientific ideas never spring from a communal body, however organized, but rather from the head of an individually inspired researcher who struggles with his problems in lonely thought and unites all his thought on one single point which is his whole world for the moment.

Max Planck

If you guys want these crazy ideas, these crazy stages, this crazy music, this crazy way of thinking, there’s a chance it might come from a crazy person.

Kanye West

When I am … completely myself, entirely alone… or during the night when I cannot sleep, it is on such occasions that my ideas flow best and most abundantly. Whence and how these ideas come I know not nor can I force them.”

Wolfgang Amadeus Mozart

The air is full of ideas. They are knocking you in the head all the time. You only have to know what you want, then forget it, and go about your business. Suddenly the idea will come through.”

Henry Ford

Inspiration comes from the Latin root “inspirare”, meaning “to breathe into”: in = “in”, spirare = “to breathe”. The word originally described divine influence; God breathing ideas into us, akin to how God blew life into Adam in the book of Genesis, and how Jesus blew the Holy Spirit into his disciples in the book of John. Inspiration eventually wandered away from its original meaning over time.

But maybe